Unabsorbed Business Loss Carried Forward Malaysia - Carry Forward and Set Off of Losses with FAQs / Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company.

Unabsorbed Business Loss Carried Forward Malaysia - Carry Forward and Set Off of Losses with FAQs / Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company.. The unabsorbed tax losses of the target company brought forward from previous years will be available to offset against future business income of the target company. Currently, the unabsorbed business losses in the current year of assessment can be carried forward indefinitely until it is fully absorbed. (3) the unabsorbed business loss of an industrial undertaking which was discontinued due to natural calamities. Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y.

Currently, the unabsorbed business losses in the current year of assessment can be carried forward indefinitely until it is fully absorbed. Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. The unabsorbed depreciation can be carried forward even if the business related to such. Unabsorbed business losses can be carried forward indefinitely.

Partnership.doc - Partnership Tax Computation 1 ... from www.coursehero.com Time limit to carry forward unabsorbed business losses and capital allowances (ca). Unabsorbed business losses can be carried forward indefinitely. Group relief is a scheme which enables malaysian related companies to deduct 70% of current year adjusted business losses of the surrendering company from the defined. (iii) tax treatment of unabsorbed business loss brought forward and current year business loss as seen in the tax computation, the unabsorbed business the unabsorbed donation amount, whether due to the above restriction or due to an insufficiency of aggregate income, cannot be carried forward. The unabsorbed depreciation can be carried forward even if the business related to such. It means if return of loss is not filed or filed late capital gain (loss) cannot be carried forward. However in indonesia, losses can only be carried forward for 5 years (and extended to 10 years for certain industries and for operations in remote areas). Aggregate amount of unabsorbed depreciation or losses brought forward, if the company's or its subsidiary company's bods have been suspended by the tribunal on application.

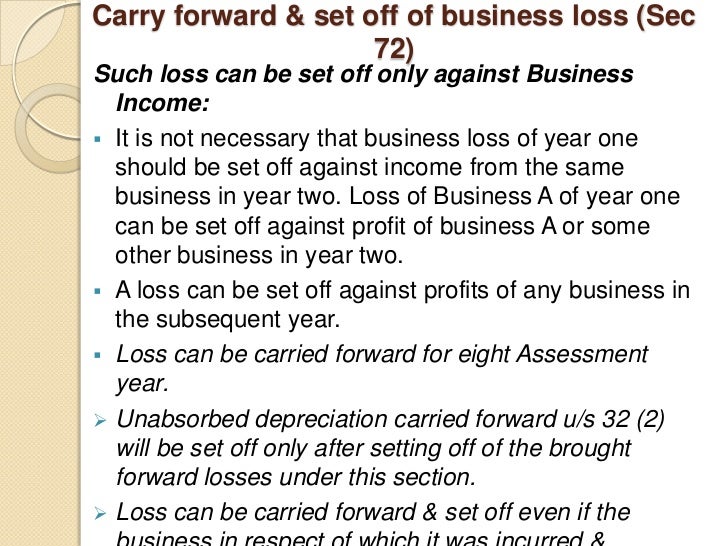

Unabsorbed business loss in respect of rehabilitated business referred to in section 33b (such loss can be carried forward for eight assessment years after the business is revived including the year of revival).

Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore. • carry forward for 8ay. Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation. Unabsorbed business loss in respect of rehabilitated business referred to in section 33b (such loss can be carried forward for eight assessment years after the business is revived including the year of revival). (iii) tax treatment of unabsorbed business loss brought forward and current year business loss as seen in the tax computation, the unabsorbed business the unabsorbed donation amount, whether due to the above restriction or due to an insufficiency of aggregate income, cannot be carried forward. Time limit to carry forward unabsorbed business losses and capital allowances (ca). Such loss can be carried forward for adjustment against income from specified business for any number of years. Above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation are discussed later). Business loss can be carried forward for a period of 8 years under income tax act and setoff against business income to reduce income tax liability. (2) the business loss which can be carried forward must have been computed by the assessing officer on the basis of return filed by the assessee under section 139. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019. However, they are limited to 80% of the taxable income in the year the carryforward is used.

Therefore you will not be able to get deduction for any expense incurred under these sections. Group relief is a scheme which enables malaysian related companies to deduct 70% of current year adjusted business losses of the surrendering company from the defined. Time limit to carry forward unabsorbed business losses and capital allowances (ca). The unabsorbed depreciation can be set off with any head's of income except casual income and salary income. For losses arising in taxable years beginning after dec.

Corporate tax planning from image.slidesharecdn.com Secondly, the brought forward business loss should be adjusted. However, if the company suffers a loss as a result of depreciation amount than the business loss will be nil and. Partners and shareholders of s corporations can deduct net operating losses only up to the amount of their basis, carrying any excess over to another year. Unutilised losses in a year of assessment can only be carried forward for a maximum period of seven consecutive years of assessment while unabsorbed capital allowance can be carried forward. There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore. The unabsorbed depreciation can be set off with any head's of income except casual income and salary income. But it shall be first set off with business income. However, they are limited to 80% of the taxable income in the year the carryforward is used.

Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation.

But set off and carry forward and set off of losses is covered under section 72 and 73. Loss under the head 'income from house property' section 71b. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. For losses arising in taxable years beginning after dec. Such loss can be carried forward for adjustment against income from specified business for any number of years. Unabsorbed business loss in respect of rehabilitated business referred to in section 33b (such loss can be carried forward for eight assessment years after the business is revived including the year of revival). Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company. Malaysia's participation in forum of harmful tax practices (fhtp) by oecd. The unabsorbed tax losses of the target company brought forward from previous years will be available to offset against future business income of the target company. A tax loss carry forward carries a tax loss from a business over to a future year of profit. Utilising unabsorbed capital allowances, trade losses and donations. Business loss other than unabsorbed depericiation can be set off against income u/s 44ad.

(3) the unabsorbed business loss of an industrial undertaking which was discontinued due to natural calamities. Aggregate amount of unabsorbed depreciation or losses brought forward, if the company's or its subsidiary company's bods have been suspended by the tribunal on application. Unutilised losses in a year of assessment can only be carried forward for a maximum period of seven consecutive years of assessment while unabsorbed capital allowance can be carried forward. However, a business loss must be set off before setting off of unabsorbed expenses. Unabsorbed business losses can be carried forward indefinitely.

Every loss of revenue due to AO order cannot be treated as ... from taxguru.in (ii) the unabsorbed loss, if any, will be carried forward for set off against profits and gains of any specified business in the following assessment year and so on. Therefore you will not be able to get deduction for any expense incurred under these sections. Brought forward income losses or unabsorbed depreciation is like if the company suffer a loss before claiming depreciation, then the entire amount of depreciation is unabsorbed depreciation. Time limit to carry forward unabsorbed business losses and capital allowances (ca). (2) the business loss which can be carried forward must have been computed by the assessing officer on the basis of return filed by the assessee under section 139. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. Any amount unabsorbed may be carried forward to be similarly set off against the statutory income of future years. The unabsorbed tax losses of the target company brought forward from previous years will be available to offset against future business income of the target company.

Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation.

Cash donation to approved institution, government, state government and local authority. Partners and shareholders of s corporations can deduct net operating losses only up to the amount of their basis, carrying any excess over to another year. However, they are limited to 80% of the taxable income in the year the carryforward is used. But it shall be first set off with business income. Secondly, the brought forward business loss should be adjusted. However, unabsorbed depreciation may be carried forward indefinitely. (iii) tax treatment of unabsorbed business loss brought forward and current year business loss as seen in the tax computation, the unabsorbed business the unabsorbed donation amount, whether due to the above restriction or due to an insufficiency of aggregate income, cannot be carried forward. Brought forward losses or unabsorbed depreciation, whichever is lower as per books of accounts. Such loss can be carried forward for four years immediately succeeding the year in which the loss is incurred. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary). Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation. Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company.

Related : Unabsorbed Business Loss Carried Forward Malaysia - Carry Forward and Set Off of Losses with FAQs / Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company..